Digital finance plays a crucial role in promoting the capability of providing agricultural finance and enabling organizations to aim for credit purpose in more precise manner.

Status of finance access in agriculture

The agriculture and food industry are facing many challenges. The global population is expected to increase from 7.6 billion in 2018 to more than 9.6 billion in 2050, which signals a significant increase in food demand (1).

Simultaneously, the speed of urbanization and the trend of shifting the economy to the indsutrial and service sectors with the exhaustion of natural resources are also big challenges for the agriculture and food industry in the future world. In particular, the financial sector in the agriculture industry will face certain impacts.

Therefore, the world’s agriculture and food industry in developing countries (occupying the largest proportion of agricultural production) needs to access a large capital to invest in machinery and improve technology, in order to increase labor productivity to meet the increasing demands while production resources are limited.

However, access to financial resources is still difficult. Investment in sustainable agriculture requires $4 trillion annually, but an estimated $2-3 trillion annually is not timely funded due to the difficulty of access (2).

Traditional financial institutions only satisfy about 5% of short-term agricultural finance needs and less than 1% of long-term needs (3). In Ugandans, more than 54% of farmers are unable to access the financial aspects, these number in Philippines is 67% (4).

Reason and solutions

In the agriculture industry, most households and small businesses are struggling to provide financial records, reports, and collateral (for example, a land mortgage may have troubles if it is unable to be clearly demonstrated or if it is in dispute), making it difficult to access capital from banks.

Due to the annual seasonal change of agricultural product, it is difficult for banks to control the records of farm operations, financial spending purposes, or the credit history of borrowers. In addition, the weather impacts make agricultural loans riskier and more complex to control.

Therefore, in order to effectively access, maintain and control these loans, banks have to spend huge operating expenses. Besides, the lengthy handling procedures and the conversion from cash to bank account is still in limitation, which have affected the borrowing demand of citizens. Cash lending also incurs many risks in terms of the management of the bank’s spending purposes.

Digital finance plays an important role in promoting the wide availability of agricultural finance services, especially in developing countries where finance access is still limited. Digital financial tools allow institutions to target credit possibilities more precisely, thereby reaching a better group of borrowers and expanding decentralized capital resources.

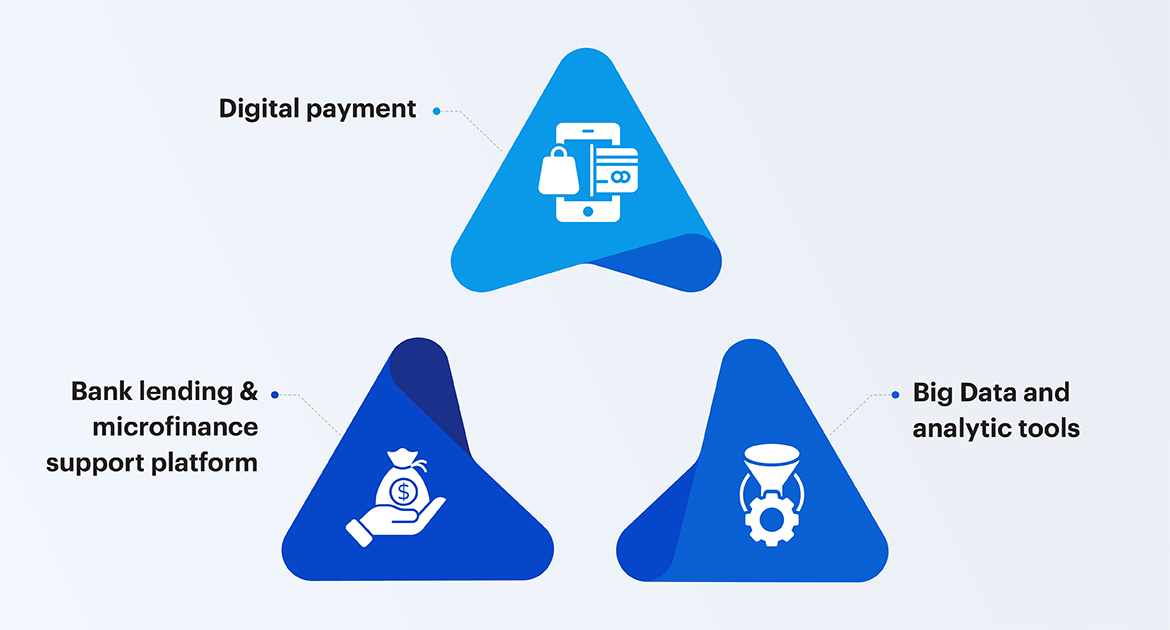

Digital financial products and services

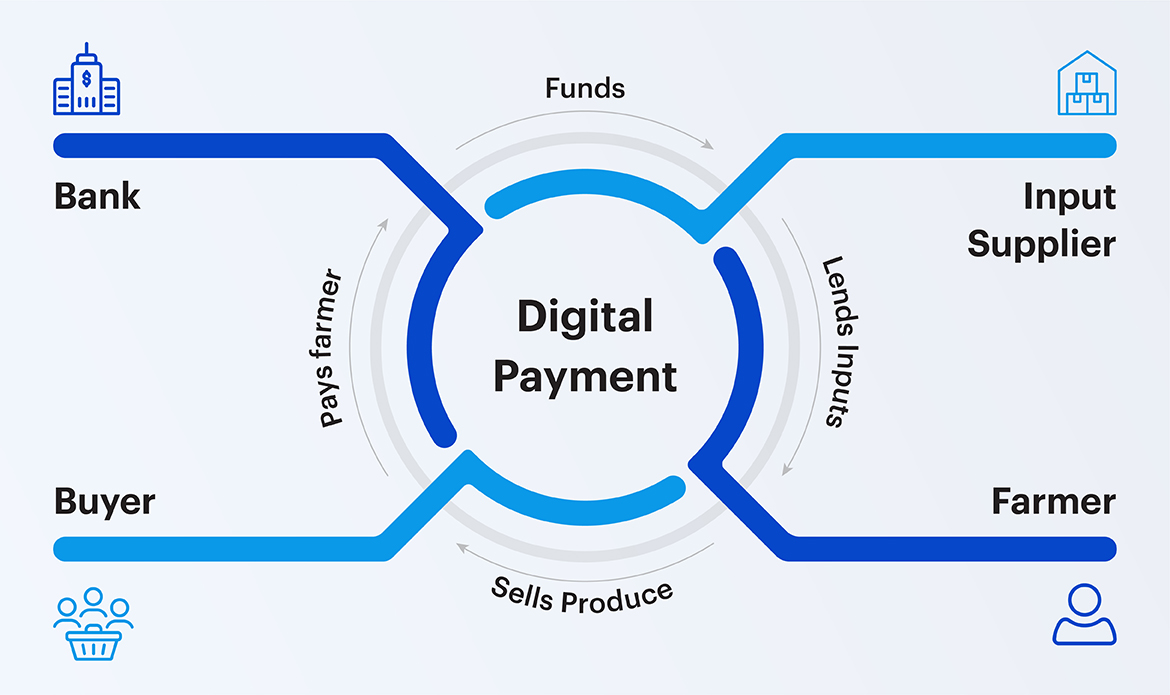

1. Digital payment

Cash payment often causes troubles, it can be delayed if bank branches are far from the farmer’s area.

In addition, cash contains many risks of fraud and improper use. Digital payment products such as e-wallets, prepaid cards, debit cards, credit cards, and mobile money are the solutions to these problems. Banks have the ability to control the flow of transactions throughout the value chain from Suppliers – Farmers – Buyers – Banks, hence, increase the efficiency of lending.

Besides, the Government’s financial support policies will satisfy citizens faster, more accurately and less fraud once digital payment methods get popular.

In Ghana, Tigo Cash mobile wallet is used to pay for small production scale farmers. These electronic payments reduce the cost and risk (fraud and theft) of cash payments. Tigo Cash is responsible for ensuring that loans are transferred to farmers for the right purpose, and Tigo agents maintain sufficient liquidity to satisfy farmers’ withdrawal demands.

2. Peer-to-peer lending and microfinance support platform

Peer-to-peer lending (P2P lending) is designed and built on a digital technology platform, using Big Data and Blockchain technology to directly connect borrowers and lenders (investors) without the participation of intermediary credit institutions.

This application has great development potentials, helping individuals and small organizations access finance solutions. The costs to manage and control the microfinance supporting platforms is much lower than the bank’s costs for the same loan.

The global peer-to-peer lending market is estimated to have a growth rate of up to 53% per year and may achieve a value of USD 490 billion by 2020. In the period 2014 – 2017, in China only, P2P loan reached approximately 1.3 trillion yuan (5).

3. Big Data and analytic tools

Fintech companies develop applications that use Big Data and analytics tools to collect data, allowing lenders to evaluate farmers to decide whether to lend or extend loans without a direct meeting request with the appraisers.

For example, Agrilife is a cloud-based technology platform developed in 2012 by Mobaha Kenya Ltd., which interacts with mobile phones and web platforms. By analyzing the data of thousands of smallholders through mobile money transactions, it is able to determine whether the small scale production farmer is eligible for credit. One of the partner banks, then, will lend to Agrilife farmers through cooperatives model.

Conclusion

The digital finance significantly reduces the supply service cost and allows the banks to offer microfinance packages to customer groups with limited budget.

This promises that under-developed countries and remote areas can grow faster from inheriting and using mobile/digital technologies to promote agricultural production. In addition, there is a huge demand in terms of national policy and strategy for the application of FinTech tools to solve agriculture problems.

References

(1) Asian Development Bank. 2019. The use of Financial Technology in the Agriculture Sector” Report.

(2) VoxEU. 2015. Financing for development: The policy and research agenda.

(3) World Bank Group. 2017. The Global Findex Database.

(4) US Agency for International Development. 2015. Mobile Solution.

(5) Global Partnership for Financial Inclusion. 2018. G20 Financial Inclusion Indicators.