In the financial sector, Banking-as-a-Service platforms have emerged as critical components of Open Banking, in which companies provide more transparent financial options to account holders by opening programming interfaces (APIs) to third parties to develop new services. What new value does Banking-as-a-Service (BaaS) bring to transform banks’ business model in the world? What are the opportunities and challenges in Vietnam?

Banking-as-a-Service platform trends

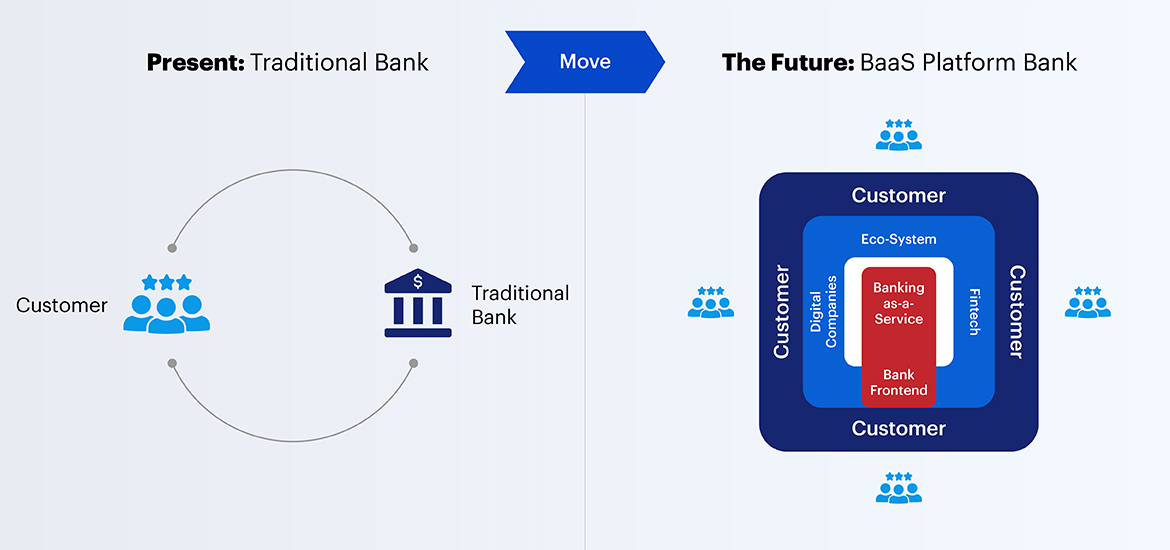

When a bank serves as a central BaaS platform, it will provide critical digital core services to third parties via APIs. This then creates an ecosystem that allows banks to work directly with customers (Bank Fronted), fintechs such as digital wallets, or non-financial digital companies in retail, energy, water,… while providing customers with convenience and security. New technologies such as Open APIs, Cloud, Microservices, and others will make it possible to actualize the BaaS platform.

The following diagram depicts the transition from traditional banking to platform banking, which serves as Banking-as-a-Service: The customer-bank connection has evolved from an one-to-one to an one-to-many relationship, enabled by the central bank functioning as a BaaS platform to promote transparency and provide better service experience for every customer.

In terms of scope, both open banking and BaaS deliver banking services through third parties via open connections or open APIs. While open banking provides non-bank enterprises access to the bank’s existing customers’ data, BaaS gives them access to the bank’s operational functions, allowing them to connect people outside the bank by integrating its services.

The Benefits of Banking-as-a-Service

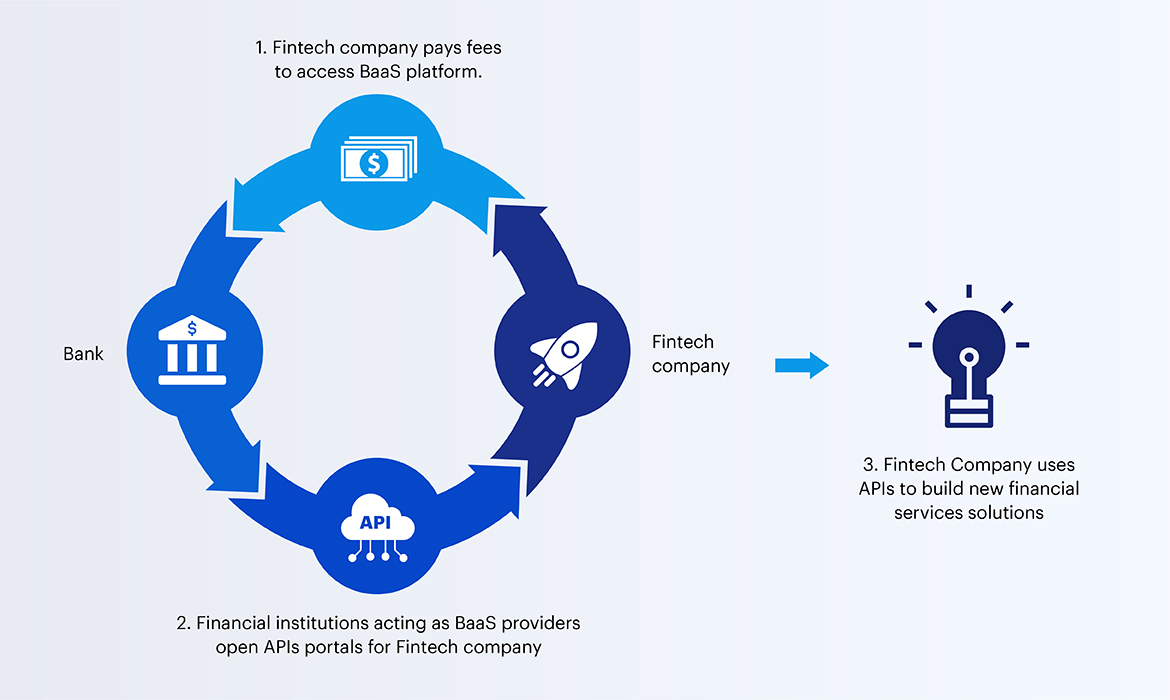

BaaS is an on-demand service that uses an application programming interface (APIs) and a cloud-based system to allow customers to access to financial services (such as payments and banking data) over the Internet. A fintech company, for example, pays a charge to BaaS providers in exchange for access to APIs. The fintech company then uses the APIs to create new financial service products for customers. When a bank functions as a BaaS provider to the community, the following diagram demonstrates how it works:

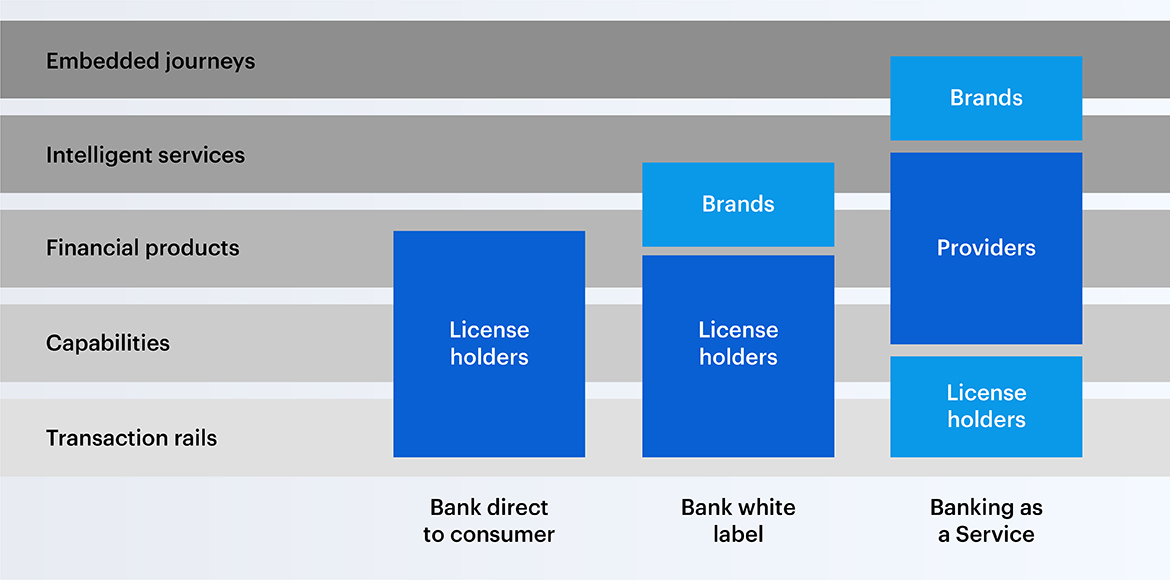

BaaS allows financial service companies to embed in a variety of software and applications. This is also known as “Embedded finance”. Nowadays, digital-based brands such as fintech are embedding financial services into their customer touchpoints, creating many opportunities to become BaaS providers. At the same time, these tech companies also realize that their talent is best spent on their core business, so they hire professionals to provide the infrastructure to run financial services on a large scale. As shown in the figure below, the BaaS wave will completely transform the banking ecosystem and financial service providers.

According to the evolution of the primary finance ecosystem, the Bank sells products and services directly to customers (Bank direct to consumer), followed by the Bank white label stage (Bank white label) – where a licensed bank will provide anonymous services to another brand of external services, and finally, the new stage is Banking as a Service (Banking as a Service). The scope of traditional banks’ licensing power decreases with each period: Initially, Bank held the right to license complete transaction rails, capabilities, and financial products, but when transitioning to the new stage, BaaS only holds the right to license transaction rails, while capabilities and financial products will be provided to the community through digital technology capable of delivering intelligent services and APIs to help companies embed then in customer’s embedded journey easier and more convenient.

There are two types of BaaS providers: Fintech companies that focus on BaaS and BaaS with banking licenses. Marqeta (fintech company) is a pure BaaS provider in the US offering debit cards and payment programs focused on card control features and real-time experience. In Europe, Railsbank (licensed bank) works with payment institutions, banks, and fintechs to issue debit cards, payments and FX through APIs. Other examples of commercial banks participating in BaaS are BBVA and Goldman Sachs. The BBVA Open Platform is an APIs-based platform that allows businesses to sell financial products to customers without handling the complete banking process themselves. Furthermore, BBVA also collaborates with Uber in Mexico. Goldman Sachs, on the other hand, announced in January 2020 that it would create an entire BaaS platform, which would be APIs-driven, cloud-native, scalable, and secure. So far, Goldman Sachs has launched a new cloud-based infrastructure for accounts and payments along with granting access through APIs, enabling developers to integrate new products into this platform easily.

In Asia, Thai commercial banks such as Siam Commercial Bank (SCB) and Kasikornbank (KBank) have started to offer open APIs functions. The Open Banking APIs include loan origination, payments, identity sharing, authentication, and check verification.

Opportunities and challenges of BaaS in Vietnam

The Covid-19 epidemic, in addition to the terrible consequences, has also accelerated the digital transformation and BaaS processes both globally and in Vietnam. This is expressed through the conclusions from data analysis according to Capgemini’s research as follows: More than half (57%) of customers now prefer Internet banking, up from 49% before COVID-19; Customers are also favoring mobile banking apps in these times of social distancing, with the number increasing to 55%, from 47% previously; The research also shows that in these uncertain times, customers are more inclined to turn to bigtech and fintech, with 30% saying they would do so because of their unhappy experience with their primary bank.

In addition, the State Bank, in Resolution No. 2655/QD-NHNN, sets the goal of introducing an Open Application Programming Interface Standard (Open APIs) by 2025 at the very latest. This is the legal and standardized basis to support the BaaS wave boom in Vietnam, substantially altering the ecosystem’s economic model. This also suggests that the BaaS market in Vietnam still remains unexplored.

Furthermore, policies relating to Open Application Programming Interface Standards (Open APIs) face challenges in terms of cloud computing services and user data security, making it critical for the banking and financial community to support and promote state agencies in developing appropriate policies, regulations, standards, or a controlled trial mechanism (regulatory sandbox) to put BaaS into practice as soon as possible.

The new wave of BaaS shapes a unique ecosystem, including Banks providing services (Providers), BaaS providers (License holders), and financial or non-financial digital brands provide more enjoyable, smarter and more transparent experience for retail customers as well as creating the opportunity to generate more value from the ecosystem. This trend is an irreversible tidal wave. Leaders in the Vietnamese banking industry need to keep up with current events, grab opportunities when barriers are lifted, and new laws and regulations are defined. When the the right time comes, be consulted to identify the most suitable strategy and prepare pioneering deployment capability with a high probability of success, laying the groundwork for a new competitive advantage.

Reference

(1) Capgemini. World Retail Banking Report 2020