The optimization by technology in every stage, especially in loan appraisal stage, has significantly reduced costs and improved customer experience due to the timely and efficient processing of the systems.

Bank credit is a convenient means of funding for consumers to buy their dream homes and for real estate businesses to complete their socio-economic development projects. However, in the banks’ viewpoint, this has also become a competitive advantage when applying high technologies to make rapid and precise decisions.

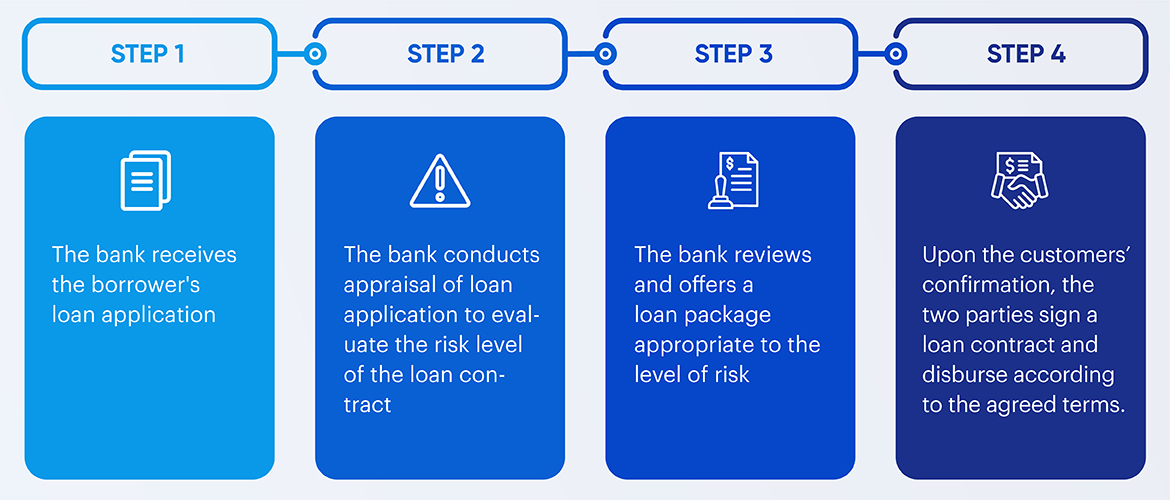

A brief overview of the loan appraisal process

Out of the aforementioned process, step 2 – loan appraisal plays a key role in assessing the offset risk premium if the borrower cannot afford the payment through his/her collateral assets. To do so, bankers often evaluate the borrower’s financial position by the 4C model:

- Capacity: includes sources and types of income as well as current liabilities of the borrower

- Capital: includes savings, investments and cash reserves

- Collateral: one or several current assets of the borrower or even the property that the borrower is borrowing to buy

- Credit: includes credit scores and credit history to assess the borrower’s ability to repay on time

Each letter “C” corresponds to a volume of papers and documents that banks or financial institutions need to collect and analyze to prove the borrowers’ position. Detail-centric is essential for bankers to make precise assessment of a loan application. Even then, there may still be inconsistencies and inaccuracies because the assessment depends on the capability of the individual assessors.

Automation in loan application appraisal – a big step forward in the banking and finance industry

Before the 2008 financial crisis, many banks competed on the basis of their high-risk tolerance through easy lending policies, even to customers with bad credit history. Today, thanks to the firm regulations of governments of different countries and the caution of banks, the competition in the field of mortgage lending is gradually shifting to focusing on the appraisal stage before granting credit. The application process requires the participation of much human-work, leading to increasing costs of each loan, which directly affects the competitiveness and profit margin of the bank. According to a study by Oliver Wyman, between 2012 and 2015, processing costs per loan increased by nearly 40% (1). As a result, digital technology is increasingly being applied to automate the loan application process in banking.

Automatic loan application appraisal is a process of applying new technology such as artificial intelligence (AI) based on big data to evaluate mortgage loan applications, thereby providing the requirements that customers need to fulfill for the approval for a loan as well as an interest rate appropriate to the level of risk that the bank will have to bear.

Fannie Mae and Freddie Mac, two of the largest mortgage lenders in the United States, are the pioneers in automated loan appraisal tools, and they have achieved outstanding results. In 1995, Fannie Mae released Desktop Underwriter software and Freddie Mac also released Loan Prospector software that applied both heuristics and statistics to process mortgage loans with less time, cost and paperwork. Despite some initial successes during those days, these software were incomplete because of the limitation in the number of data samples. Today, AI and machine learning-applied data models have allowed algorithms to evaluate loans more accurately than manual appraisal because machine learning models provide results by combining a large volume of observations in the data set, especially for standard loans.

Rocket Mortgage (formerly Quicken Loans) has become the largest retail lender in the United States thanks to its strategy of relying on wholesale funding to make loans as well as using online lending processes instead of branch system. Rocket Mortgage has an ability to analyze a loan application in approximately 10 minutes, which becomes a niche advantage for both credit officers and applicants. Besides, a series of other mortgage lending companies have also applied and improved their own automated underwriting software to compete in this market. Automation has partly helped banks gain profits by cutting personnel costs, and at the same time, improving customer satisfaction due to timely and efficient processing systems.

The future of loan appraisers

Although the automatic appraisal of mortgage loan applications has effectively supported the loan application approval process of banks, digital tools are not fully complete, especially non-standard or personalized loan applications still require the participation of human-work appraising procedures. Therefore, many fintech startups are developing solutions to achieve a fully automated appraisal model, in which borrowers no longer need to talk directly to appraisers.

From the borrower’s perspective, real estate is highly-valued assets and the complexity of the mortgage process requires the assistance of experienced professionals. After all, borrowing – lending is a potentially risky process and it requires absolute trust between the parties involved, so mortgage lending business may still need social relationships and human interactions. That explained why Wells Fargo, who have invested $500 million applying the digital mortgage experience but about three-quarters of their homebuyer customers still expect expert assistance throughout the loan process (2).

This means, at least in the medium-term future, humans will still play an important role in the mortgage lending experience, but at the same time, banks and financial institutions also need to accelerate the automation of this process if they want to create a competitive advantage in the 4.0 era. Some areas where mortgage lenders can go digital including but not limited to Digitizing records, documents and automatically extracting necessary data; Automating error-prone manual tasks; Consolidating customer information between communication channels, avoiding asking questions that customers have provided answers for, etc. As a result, bankers could focus on their higher value-added tasks such as sales and customer service.